Phillips Curve Breaks Down Under High Inflation

Commentary

International organizations such as International Monetary Fund (IMF), World Bank (WB), and Organization for Economic Co-operation and Development (OCED) have revised upward their economic forecasts in turn. Were their forecast updates correct, this would mean the global tightening is not strong enough, and probably not enough to bring down inflation to the 2 percent target. Data show this is indeed the case. Most countries, including United States, nations within the eurozone, the United Kingdom, and Australia are having their core inflation rates stayed flat (and high) over the past three to six quarters.

The theoretical basis of suppressing inflation by tightening is via the demand channel. Recently there are central bank research pieces attributing inflation to supply shocks. No doubt there were two to three years ago, but certainly not by now. This line of reasoning can hardly explain the flat inflation trend over the past year or so. And if this had been the case, central banks should not have tightened in the first place because monetary tools cannot solve any supply problem. Their deeds (tightening) have indeed refuted their words (research).

If inflation remained high via the demand channel, then the series of monetary tightening should (and have to) cool down not only inflation but also the real sector. As both inflations remain high and the unemployment rate remains low, one cannot simply argue the Phillips curve (which prescribes an opposite relationship between the two) has broken down. Nevertheless, how much the trade-off between the two is subtle. Central bankers rely heavily on such an exact relationship, yet it is never stable over time, as literature has documented long ago.

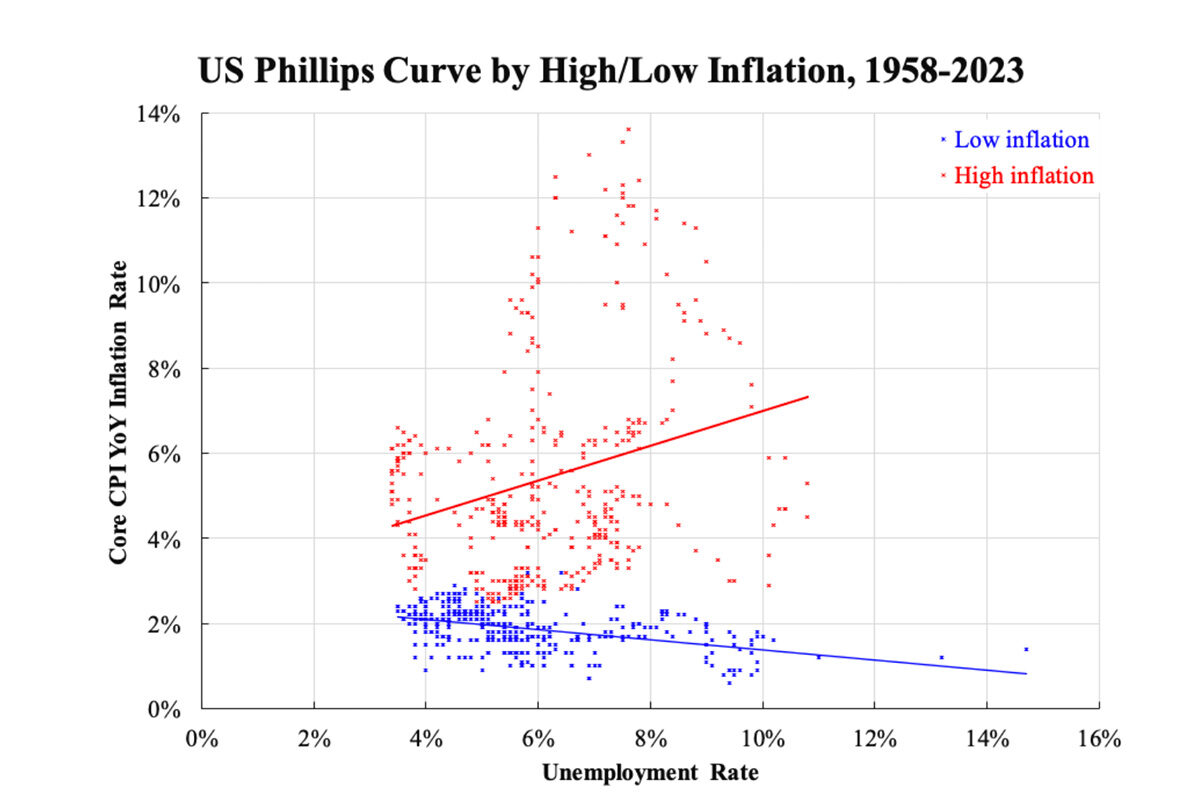

To see this, the accompanying chart shows the oldest naïve version of U.S. Phillips curve. To eliminate the volatile inflation components, core inflation is used. The new thing here is to break down the whole period from 1955 to now into two episodes by whether inflation is high—by “high” here means core inflation is higher than 2.4 percent, which cannot be rounded off to 2 percent. The conclusion is when inflation is normal enough, then monetary policy is effective in trading it off from unemployment. When inflation is out of control, however, the trade-off breaks down.

Ignoring the red trend line which does not fit the red dots, a glance over the data suggests the relationship is highly uncertain when inflation is well above 2 percent. In other words, we cannot tell whether inflation will be contained by having higher unemployment, or how much employment has to be sacrificed for a target inflation. As the standard argument goes, this is inevitably the cost of high inflation, because the price level is the means of demand and supply signal transmission and it cannot perform such function well when it becomes volatile.

Accordingly, all central bankers will tell you that they will have to decide meeting by meeting—meaning that they do not even have a clear idea about the short-term economic outlook. As monetary policy goes with long lagged effect, they will likely commit a mistake of either not doing enough or overdone.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.