Don’t Fear Central Bank Digital Currency, Embrace It Instead

Distressed Patriotic Flag Unisex T-Shirt - Celebrate Comfort and Country $11.29 USD Get it here>>

There are important economic, competitive, and geopolitical reasons to adopt a US CBDC

Commentary

Last week, South Dakota Republican governor Kristi Noem rejected a bill (HB1193) to update the Uniform Commercial Code (UCC) with her own unique “brand” of veto. The veto came because Noem opposed the bill’s language outlawing Bitcoin and other cryptocurrencies, but allowing a central bank digital currency (CBDC), which is issued by governments.

Noem objected both to cryptos like Bitcoin being made illegal and to CBDC being made legal. She’s wrong on both counts.

I VETOED HB 1193. This bill adopts a definition of ‘money’ to specifically exclude crypto like Bitcoin. And it opens the door to the risk that the federal government could adopt a central bank digital currency.

South Dakota will always stand for Economic Freedom. pic.twitter.com/yqN2mPPaLj

— Kristi Noem (@KristiNoem) Mar. 10, 2023

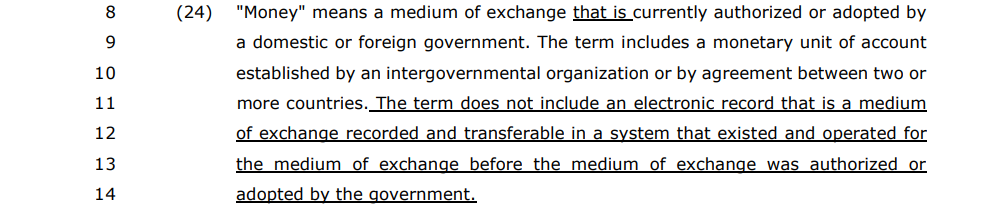

The intent of the bill is best summarized from the bill text itself:

In other words, cryptocurrencies like Bitcoin would not qualify as “money” because it “existed and operated … before the medium or exchange was authorized or adopted by the government.” But a “medium of exchange” that is an “electronic record” “authorized or adopted by the government” would be money.

Cryptocurrencies

I’ve written several times elsewhere about my almost rabid disdain for cryptocurrencies. I see them as vacuous, akin to a Ponzi scheme benefiting the creators and early adapters, but only for a short time. I’ve refuted the assertions of those who support cryptos at some length elsewhere, I won’t repeat those objections again here.

CBDCs

But as I strenuously refute cryptos, I am vociferous in my support of government-backed CBDCs for economic, competitive, and geopolitical reasons. If the United States fails to adopt a CBDC, I believe it will ultimately risk American prosperity and, possibly, even the republic itself. America’s failure to adopt CBDC, and soon, could eventually rise to be an existential risk to the country.

CBDC Is ‘Next’

Economically, in the second decade of the twenty-first century, it is essential that financial transactions be completed instantaneously and without intermediaries. Various private entities, like Amazon, have tried—and some have achieved—that goal. But a CBDC, bearing the imprimatur of the United States of America, will expedite the flow of commerce, including commerce across national borders and even possibly effect a conversion of foreign currency. I can remember as a young teenager, 50 years ago, traveling with my family to Europe and my father having to load up with travelers’ checks, his credit cards, and a bank letter of credit to ensure we had cash overseas. Today, of course, my bank ATM card will spit out local currency in virtually any major city in the developed world, do the conversion, debit my bank account for the U.S. dollar equivalent on the day of the withdrawal, and charge a small fee (that my bank waives above a deposit balance threshold).

But we need to take commerce to the next step: no ATM card, no credit card. Instead, just a secure CBDC account that I can use in Boise, Boston, or Berlin without a middle man, and without a fee. Further, it should be available for multinationals to transmit millions of dollars for goods, services, and financial transactions as well as for tourists at a Vatican souvenir shop.

We Have No Choice but to Adopt a CBDC

Toward the end of World War II, the Nazis had invented jet aircraft. With Germany defeated, theoretically, the world could have simply continued to use propeller-driven aircraft. But the technology was “out there”; we had to develop jet aircraft simply because someone—the Russians, the British, the French—would (and did).

CBDC is much the same. Our competitors will proceed with CBDC; it is inevitable. The world of government fiat money being paper has passed, as this interactive chart from the Atlantic Council illustrates.

China’s central bank, the People’s Bank of China, already has a CBDC, the e-CNY, in circulation that they treat as what economists call “M-0” (M-Zero), which is, essentially, the equivalent of cash in your pocket and bank cash reserves. According to the Atlantic Council, the e-CNY

“… is further ahead of many other advanced countries, who are still only researching CBDC development. China’s interest in the cross-border functionality of the e-CNY and its relatively advanced stage of development position it well to set standards in CBDC developments globally. That is the role that China is eager to play, according to our (research).”

The first big test of the e-CNY was at the 2022 Beijing Winter Olympics, where the only means of transacting business were by cash, Visa cards, and e-CNY.

As the “first to market” with a CBDC, China hopes to set the global standard for how the technology is integrated. The United States and other democratic nations need to be in the marketplace to offer an alternative and to defeat China’s ambitions.

I expressed grave concerns about a CBDC in these pages more than a year ago. But my concerns were more about the totalitarian Chinese Communist Party regime’s control of it than any inherent concerns about the technology. Yes, a CBDC could allow tracking of individual expenditures and where you spend your money. But in a “rule of law” society, that should be permitted only under a subpoena, just as it is today with your bank records, credit and debit card records, EZ-Pass records, etc. (If you are concerned about whether we are still a rule of society, I share those concerns, given recent revelations about FBI and Justice Department abuses. But that discussion is beyond the scope of this article.)

Concerns that the Federal Reserve could, theoretically, cancel some or even all the funds in your digital wallet are valid. That has been discussed as a means for the Fed to cross the “zero lower bound.” That would work as a means to further reduce interest rates, even below zero, to encourage you to spend your money as a means of stimulating a moribund economy. Negative interest rates would be achieved by reducing the balance of your CBDC digital wallet under a “use it or lose it” notion. But the Fed already does something akin to that with bondholders: if you buy a Treasury bond with a $1,000 face value paying 2 percent interest, and the Fed raises rates to 3 percent, you will have lost a portion of the value of your bond, unless you hold it to maturity. Breaking through the zero bound is the same thing, except that instead of tightening the economy, the Fed would be stimulating it.

Besides, the fears about a CBDC can be said of other forms of currency, too. India, for example—a democratic, rule of law, republic—canceled its then existing currency in circulation in 2016 with just hours’ notice in order to flush out India’s underground, untaxed, economy. Banks were prohibited from dispensing more than a nominal amount of the new currency for daily expenses. In order to realize the value of any currency that had been prohibited (and that some had hidden from the tax man), Indians had to deposit it in a bank and receive new currency at par value of the old currency they had deposited. The exercise disrupted the Indian economy, but achieved its policy goals.

CBDC Is a Geopolitical Necessity

SWIFT is an acronym for the Society for Worldwide Interbank Financial Telecommunications. For the last 50 years, it has enabled international and bank-to-bank financial transactions in a fast, efficient manner. It has been an enormous success in speeding payments.

SWIFT has also been a success as the principal means by which the United States imposes financial sanctions on offending and recalcitrant foreign despots. And that may have been the problem; it was the impetus for our leading adversary nation—China—to find a work-around like the e-CNY. Others will do the same. Iran and Venezuela, for example, have CBDC coins in progress; there is talk of an OPEC coin. There is even some talk that each of these nations, including U.S. adversaries, are planning to make their CBDC commodity money—that is, money backed by gold or oil. For many, this commodity money is superior to fiat money, notwithstanding commodity price fluctuations.

If we and the world hope to step away from China as a manufacturing base, and to move to other low-wage producers, we’ll need to adopt CBDC to be able to make payroll, purchase supplies, and engage in other financial transactions in remote, far-flung, un-banked regions of the world. In places like Africa, Latin America, and Central and South Asia, where there are critical rare earth elements needed for chip manufacturing, and even in venues for low-wage manufacturing generally, a CBDC will be necessary if we hope to effect payments without first building the hard currency banking infrastructure that would otherwise be needed.

Summary

First, policymakers should ignore disingenuous “concerns” about a CBDC raised by people who have holdings in Bitcoin and other cryptos; they should be dismissed out of hand. A U.S. dollar CBDC would likely eviscerate the value of Bitcoin and other cryptos the instant it hit the market. Arguments by Bitcoin advocates against CBDC are the equivalent of the owner of the town horse stable against “horseless buggies.” Their concerns aren’t about policy but profits. Ignore them.

While there are certainly risks associated with the United States adopting a CBDC, those risks are almost exclusively a function of trust in our government. But trust in government should be addressed separately as to whether the United States should adopt a CBDC. While doubts about that trust certainly exist, given the power of the administrative state, most of whatever restrictions government could impose on a CBDC could also be imposed on paper currency—and customer access to it—as well.

Ultimately, governments control the mediums of exchange that can be used by the people in their jurisdiction. In this second decade of the twenty-first century, America should not be beholden to the electronic currencies of a China, a Venezuela, or any other nation to operate successfully in the global economy. If we are to continue to lead the world, we must be second to none in CBDC.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.