Don’t Confuse Cycle With Trend

Commentary

Since the fadeout of the first round of the banking crisis, the market has calmed down as if nothing had happened. Recession probability edged up, but most believe advanced economies would be in more trouble than emerging economies. This has also been the standard tone of international organizations like the International Monetary Fund (IMF). In their latest outlook, they are also more bullish on emerging economies in quite many aspects as usual. However, casual observation suggests this is not the case if we focus on bust rather than boom.

Regarding emerging economies similar to third or fourth-tier stocks (growth stocks) and advanced economies as the first or second-tier, growth stocks tend to be volatile and perform much better in bull but much worse in bear markets. The underlying reason for high volatility is the high leverage behind them. Emerging economies and growth stocks are alike because their gearing ratios are higher than advanced economies or large caps. Naturally, the magnitudes are magnified, whether in the up or down direction, happening in boom (bull) or bust (bear) markets.

In finance, bearing additional risks might bring extra returns. The growth stocks might therefore outperform in the longer term. The same principle applies to emerging economies. However, such long-term better performance is a trending phenomenon rather than a cycle. Growing stocks or emerging economies are volatile by construction, which refers to the upside and the downside. Some fund managers and even the IMF cannot distinguish such simple differences and confuse trend outlook with cycle outlook, especially when discussing bear market or recession.

Historically, crises were more prone to happen in emerging economies. Beyond volatility, another reason might be that they are situated in a passive position. As emerging economies perform more like sellers (supply) than buyers (demand), they are more passive in front of recession because most recessions in history were due to adverse demand rather than supply shock. Another aspect, apart from the source of the shock, is the lack of international currencies, so counter-cyclical policies tend to follow the advanced economies. Those policies might not fit.

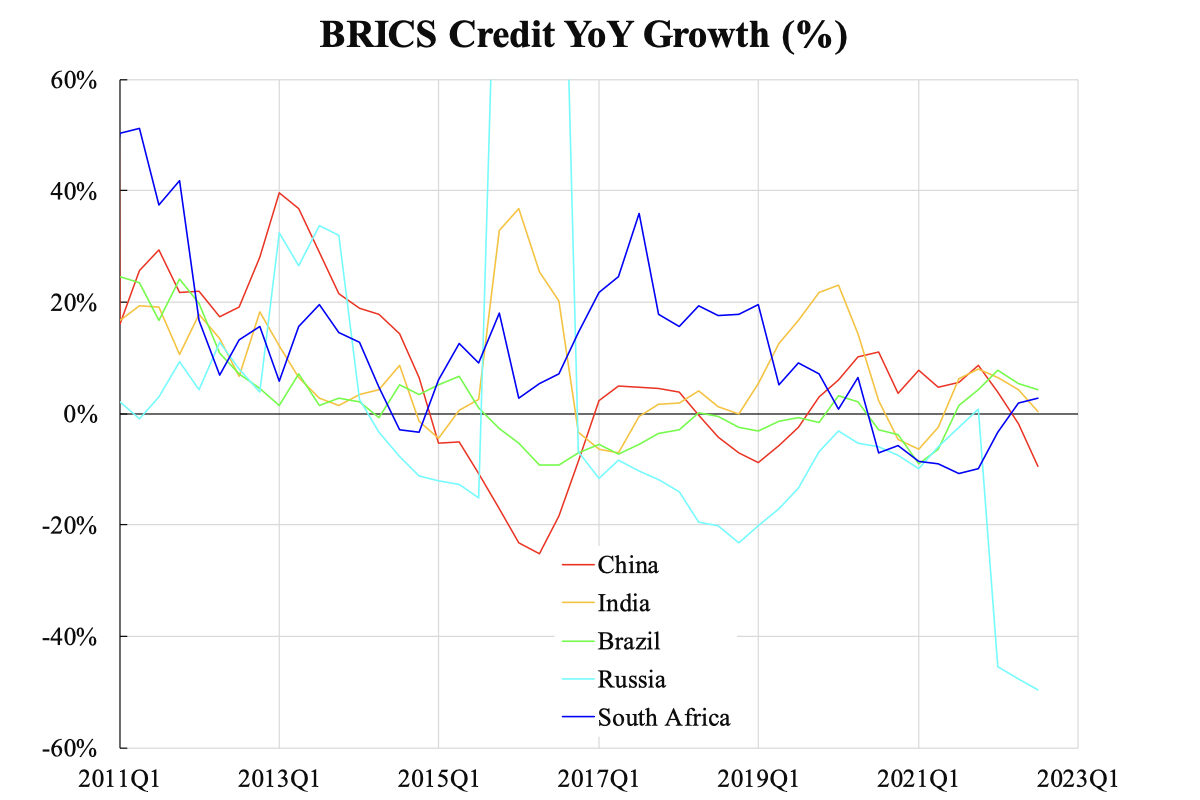

The accompanying chart shows the credit plus loans year-over-year (YoY) growth of the BRICS as compiled by the Bank for International Settlements (BIS). The downtrend has not changed since the financial tsunami in 2008 and the European debt crisis in 2012. The so-called recent rebound did not exhibit in this set of data. Slow credit matches weak inflation. India, Brazil, and Russia have only 4-6 percent YoY inflation at the latest, which is low from the standard of emerging economies. China is even lower and is now on the brink of deflation.

The experience of post-1990 Japan and post-2008 U.S. conclude that weak credit is a knotty problem. Printing money or massive injection will not help. Only time can heal when debt and other deleveraging happen enough. Now is a respite because Western markets have not yet entered a recession, but the situation can worsen as quickly as it arrives. the IMF will be proved wrong again in their latest outlook.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.